View all articles

INTEREST RATES HAVE FINALLY DROPPED IN THE US AFTER A DOUBLE-BARRELLED CUT. BUT WILL THEY FALL AS FAST FROM HERE AS INVESTORS EXPECT?

View all articles

September 23, 2024

The fed goes big

INTEREST RATES HAVE FINALLY DROPPED IN THE US AFTER A DOUBLE-BARRELLED CUT. BUT WILL THEY FALL AS FAST FROM HERE AS INVESTORS EXPECT?

The US Federal Reserve (Fed) delivered a ‘jumbo’ cut to interest rates of half a percentage point, taking the benchmark borrowing rate to the range of 4.75% to 5.00%. While a decrease was expected by virtually everyone, the question was the quantum. Opinion was fairly evenly split on whether it would be 0.25% or 0.50%.

Digesting the news, the US stock market wobbled a bit at first but ended the week up. This is what you would expect, given a fall in rates tends to be good for the prices of stocks as long as there’s no whiff of recession in the air. When prevailing rates fall, it makes companies’ expected returns look more attractive relative to cash and other lower-risk assets, encouraging people to buy them. However, if recession is in the offing, the calculation changes. Because downturns tend to mean fewer sales and worse profits (and even a swing to losses in some cases), they hit stock prices hard.

Counterintuitively, US government bond markets took the news slightly negatively – the 10-year Treasury yield ended the week about 10 basis points (10 hundredths of a percent) higher, meaning that its price fell. Typically, a fall in a central bank’s benchmark borrowing rate would boost that nation’s government bond prices, pulling down its yield. Yet US Treasury yields, both short-term and longer-term, had fallen significantly ahead of the Fed’s decision. After the cut, many investors focused on the Fed committee’s plans for future rate cuts: was this the start of a rapid fall or would rates take a while to fall?

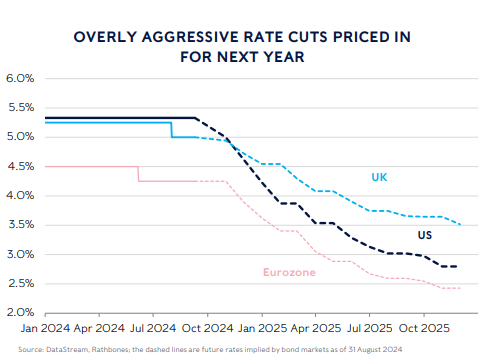

Bond investors and the Fed committee were not seeing eye to eye on that question before last week’s monetary policy meeting and they certainly haven’t aligned themselves since. Despite the big first step in cutting rates, the Fed has outlined a relatively slow path from here. The latest iteration of the ‘dot plot’, which maps committee members’ forecasts for interest rates, shows the average member expects the benchmark rate to be about 4.75% by the end of the year. Investors, as implied by interest rate markets, believe it will be 4.25%. Similarly, the average Fed member thinks the rate will be somewhere around 3.25% by the end of next year; investors assume it will be comfortably below 3.0%.

Now, Fed members have been wrong before! Yet so have investors. For now, we think the Fed’s more sedate pace of cuts is the most prudent forecast. While the US jobs market has cooled substantially over the past few months, it’s still nowhere near ‘bad’ territory. And it’s hard to argue that the US economy is tanking either: the last official GDP growth was 3.00% in the second quarter and the unofficial-but-less-lagging ‘nowcast’ estimate from the Atlanta Fed suggests Q3 growth is 2.9%.

While we expect the US economy will slow from here, we think a recession is not the most likely outcome. If we are correct, that should be good for stock prices, as rates fall and profits aren’t upended by a contracting economy. It should benefit bonds as well, although they have already posted gains in anticipation, so they may be a bit rockier in the coming months – at least until they come to an agreement with the Fed’s view of the world.

A sterling run

At its monetary policy meeting last week, the Bank of England (BoE) kept its benchmark rate where it was, at 5.00%. Unlike the Fed, which must aim for full employment and price stability (which it interprets as core PCE inflation of 2% over the long term), the BoE’s primary objective is a 2% target for CPI inflation. While UK CPI inflation remained at 2.2% in August, services inflation re-accelerated from 5.2% to 5.6%. Core inflation (which strips out volatile energy and food prices) also increased, from 3.3% to 3.6%.

While the BoE doesn’t set out its rate forecasts like the Fed, the policy committee has been pretty clear that it still expects rates to fall steadily from here. However, that drop may be slower than elsewhere as everyone waits for services inflation to cool. Investors are assuming that rates will hit 3.5% by the end of 2025. We think that it’s at least as likely that rates won’t fall as fast in the UK as markets imply. Unless, that is, a recession or other shock arrives, which, as the last two months of retail sales reminds us, is unlikely to be around the corner.

Because the prevailing UK interest rate is shaping up to be relatively high and fall slower than elsewhere, it’s helped boost the value of the pound. Sterling is buying €1.197 and $1.332, the highest the pound has been against either the euro or the dollar in two and a half years. Just a shame it got there after the summer holidays. Hopefully it remains strong when it comes time to book holidays for some winter sun!

The views in this update are subject to change at any time based upon market or other conditions and are current as of the date posted. While all material is deemed to be reliable, accuracy and completeness cannot be guaranteed.

This document was originally published by Rathbone Investment Management Limited. Any views and opinions are those of the author, and coverage of any assets in no way reflects an investment recommendation. The value of investments and the income from them may go down as well as up and you may not get back your original investment. Fluctuations in exchange rates may increase or decrease the return on investments denominated in a foreign currency. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated.

Certain statements in this document are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend upon or refer to future events or conditions, or that include words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “intend,” “plan,” “believe,” or “estimate,” or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are by their nature based on numerous assumptions. The reader is cautioned to consider the FLS carefully and not to place undue reliance on FLS. Unless required by applicable law, it is not undertaken, and specifically disclaimed that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events or otherwise.