Tower REITS Drive Margins and Return on Capital

Publicly-traded Tower real estate investment trusts (REITs) generally own a network of vertical tower structures upon which their tenants place their communications equipment. Their tenants are large telecommunications firms (i.e. AT&T, Verizon, Sprint) that provide cellular phone service and plans to consumer and business clients. These tenants enter into long term leases with the Tower REITs to host their equipment on the REIT’s towers. Competing telecommunications firms often host their equipment on the same towers in order to leverage the capital investment of the Tower REITs

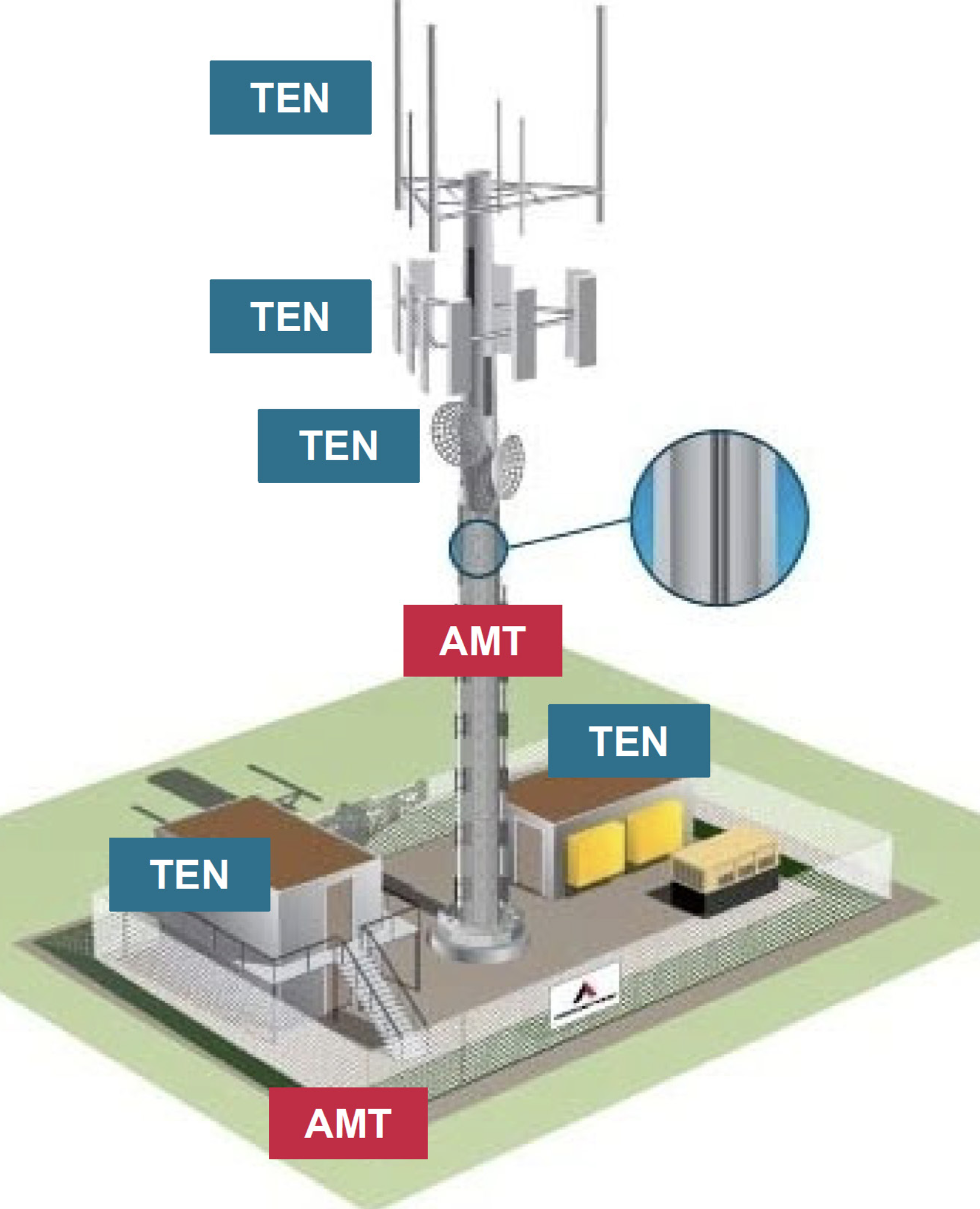

Operated by Tenant (AMT)

- Tower structure – our tower sites are typically constructed with the capacity to support ~4 - 5 tenants

- Land parcel owned or operated pursuant to a long-term lease by American Tower

- American Tower owns generators at some sites to help facilitate back-up power for the site’s tenants

Operated by American Tower (TEN)

- Antenna equipment, including microwave equipment

- Tenant shelters containing base station equipment and HVAC, which tenants own, operate and maintain

- Coaxial cable

Source: American Tower.

This arrangement benefits both parties as the telecommunication firms can offer similar national coverage networks without having to fund large capital expenditures. The Tower REIT benefits from increased utilization of their tower network, which drives margins and return on capital.

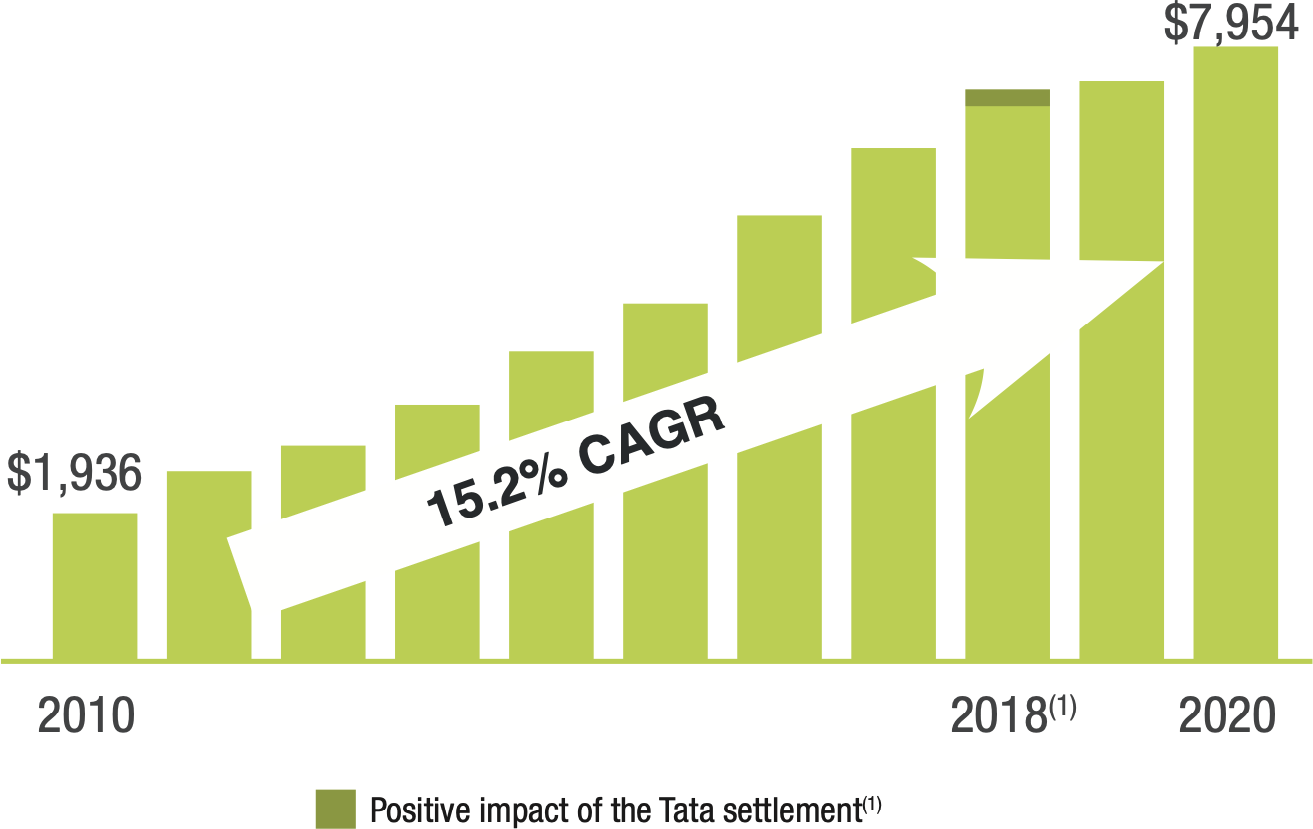

Total Property Revenue

($ in Millions)

($ in Millions)

Source: American Tower.

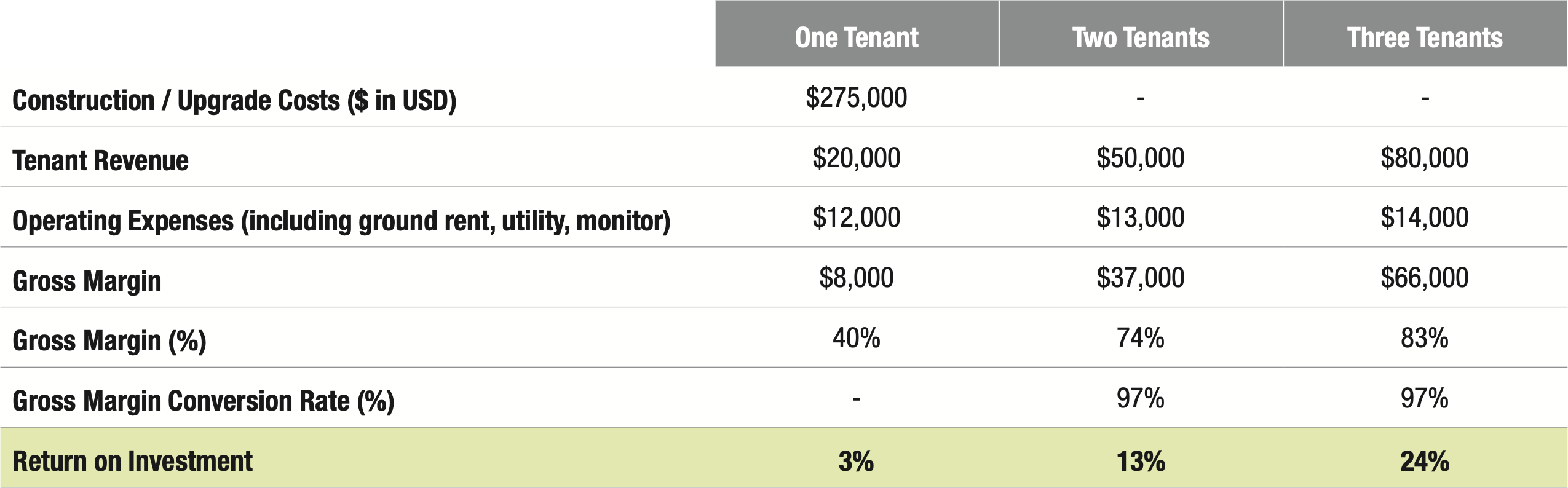

American Tower operates a global portfolio of over 170,000 communications sites in over 15 countries. In the US, American Tower’s tenants enter into five to 10-year leases with annual 3% escalators. Return on Investment is tied to tenant concentration and rises from 3% for one tenant to 13% for two tenants to 24% for three tenants, with Gross Margins rising similarly from 40% to 74% to 83%.

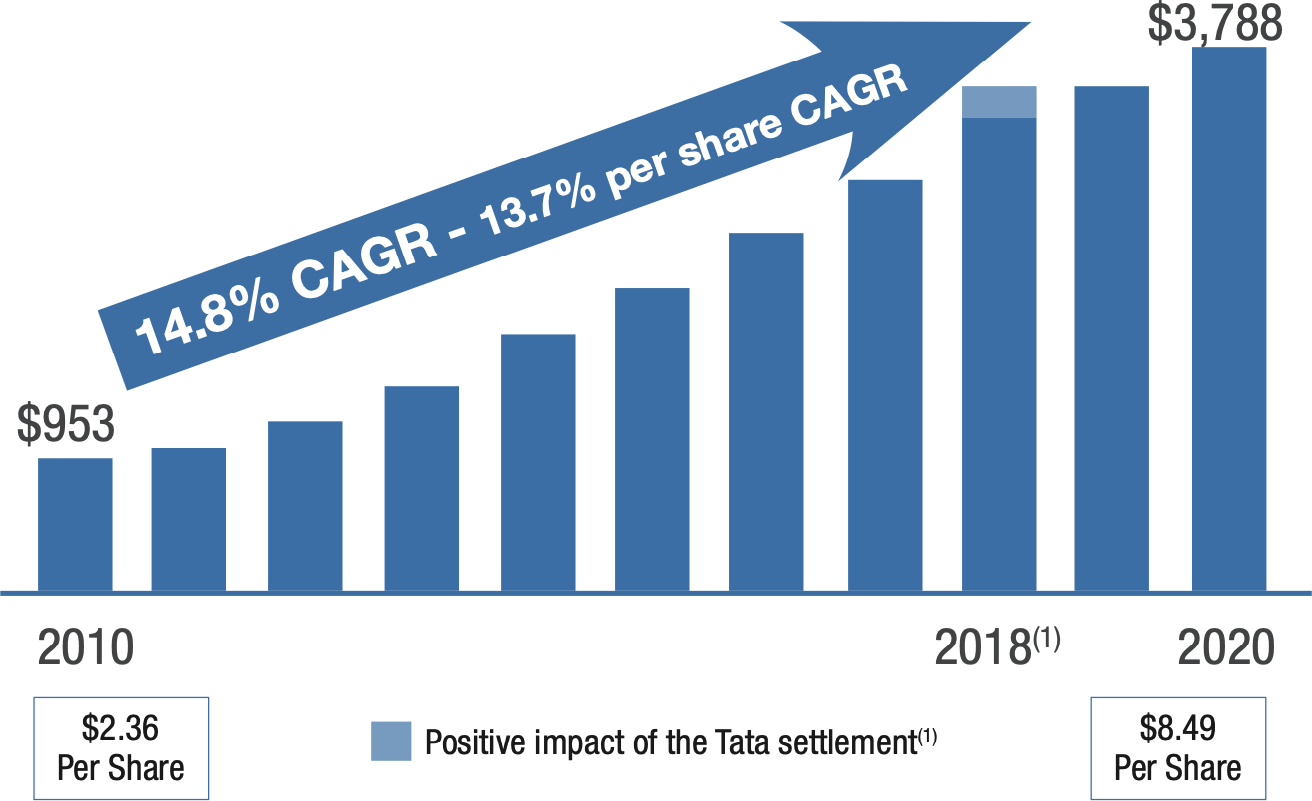

Total Property Revenue

($ in Millions)

($ in Millions)

Source: American Tower.

Demand for the towers is driven by macro trends such as the Internet of Things, social media, e-commerce and smart phone penetration. The industry enjoys high barriers to entry (scale, capital, locations) which supports the oligopolistic industry structure globally. Finally, the tower networks are mission critical infrastructure for the telecommunications firms without which, they cannot operate their businesses.

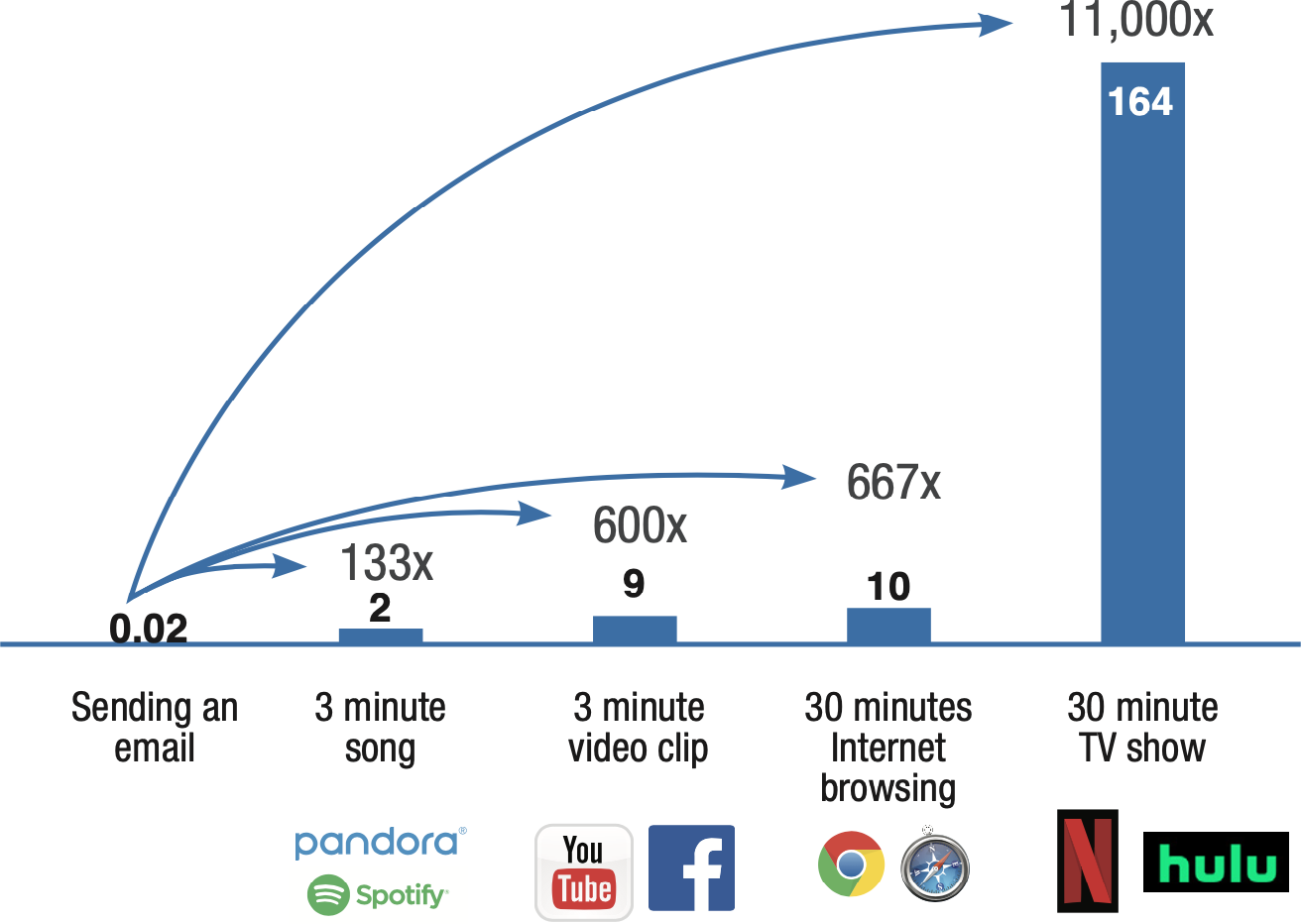

Average Data Used by Activity

(in megabytes)

(in megabytes)

Source: American Tower.

Tower REIT revenue growth is largely driven by increased data usage by an increasing number of smart phones in circulation. While smartphone unit sales have begun to slow, per capita data consumption continues to grow rapidly. Telecommunications firms add to this momentum by offering more unlimited data plans to subscribers. This in turn drives data usage which drives the need for larger and denser networks to handle all the data traffic. The economies of scale provided by expanding the network drives margin expansion and return on investment for the Tower REITs.

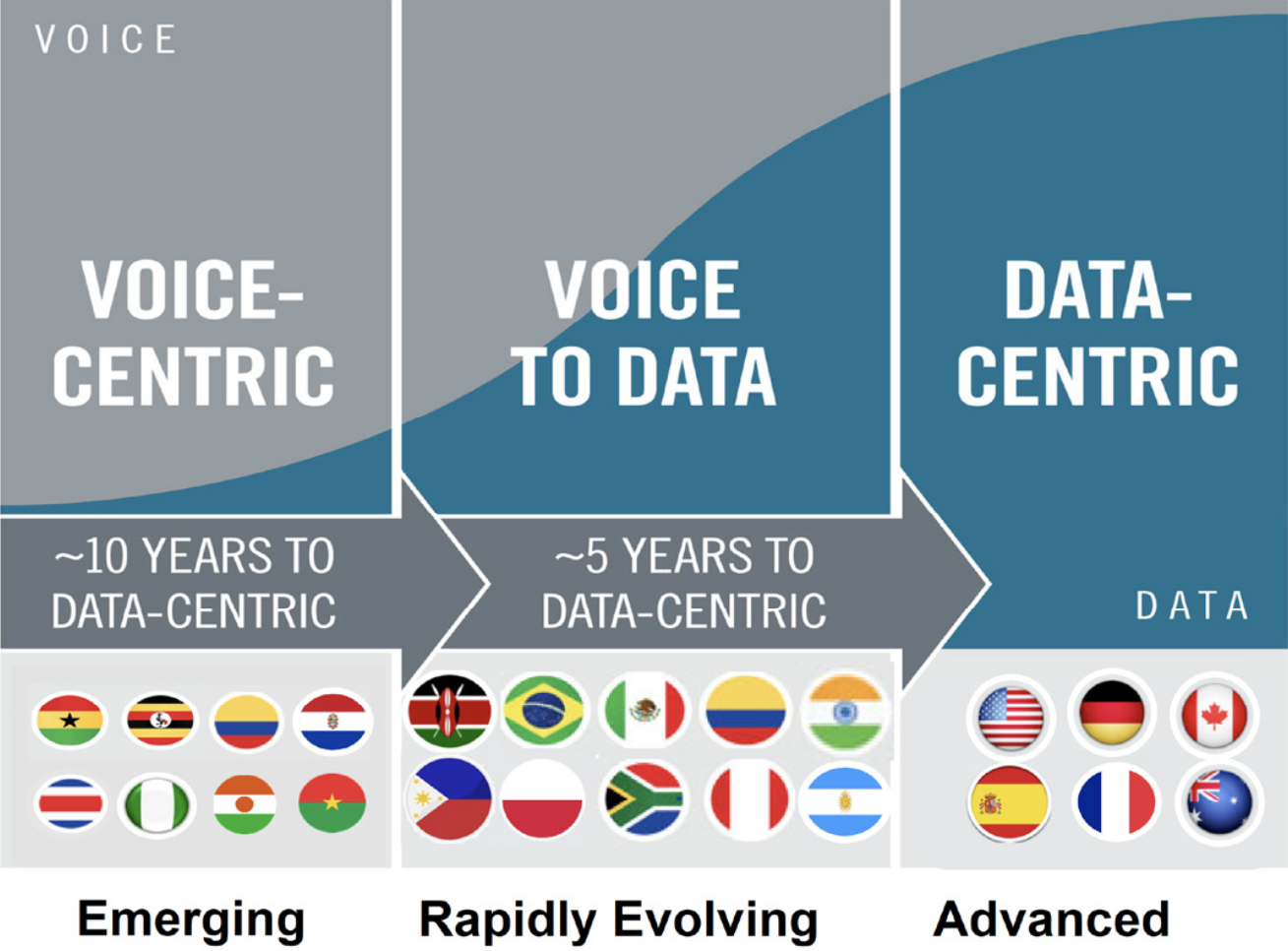

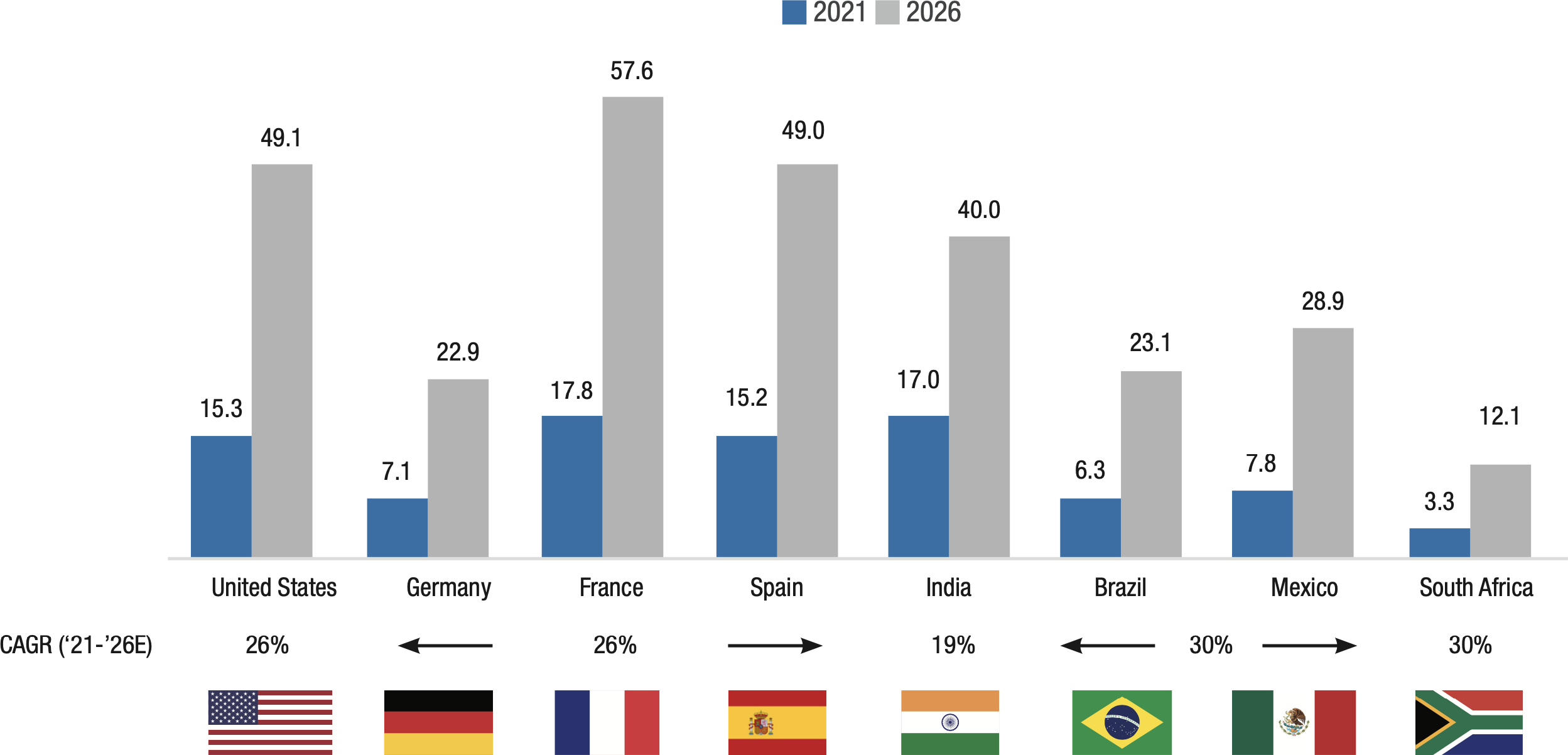

While the U.S. market is a mature smartphone market it still offers tremendous growth potential as data usage continues to grow. Other developing markets such as India, Brazil and South Africa represent even greater growth potential as their populations continue to grow while smartphone penetration and data usage also grow.

While the U.S. market is a mature smartphone market it still offers tremendous growth potential as data usage continues to grow. Other developing markets such as India, Brazil and South Africa represent even greater growth potential as their populations continue to grow while smartphone penetration and data usage also grow.

Average Monthly Smartphone Data Usage

(in gigabytes)

(in gigabytes)

Source: American Tower.

Internet access on mobile devices and their applications continues to grow with needs for greater bandwidth to fuel content rich platforms and ‘always-on’ tools such as social media and home automation.

Source: eDiscovery Today.

The economics of tower development are attractive and benefit from significant economies of scale. In the U.S., cell towers can generally be built for $275,000 at a cap rate of 7%. Cell towers with one tenant generate Gross Margins of 40% and an ROI of 3%. However, the addition of the second or third tenant drives significant cash flow and return growth.

Once the cell tower has two or three tenants it can be sold for a multiple of its cash flows (“Adjusted Funds From Operations” or “AFFO”). In the current market, U.S. cell towers are being acquired for 30x to 34x cash flow while U.S. cell tower REITs (American Tower Corporation, Crown Castle International Corp., SBA Communications Corp.) trade between 25x to 35x AFFO.

Once the cell tower has two or three tenants it can be sold for a multiple of its cash flows (“Adjusted Funds From Operations” or “AFFO”). In the current market, U.S. cell towers are being acquired for 30x to 34x cash flow while U.S. cell tower REITs (American Tower Corporation, Crown Castle International Corp., SBA Communications Corp.) trade between 25x to 35x AFFO.

U.S. New Macro Tower Build Economics Drive Strong ROI

Source: eDiscovery Today.

Certain statements in this document are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend upon or refer to future events or conditions, or that include words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “intend,” “plan,” “believe,” or “estimate,” or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are by their nature based on numerous assumptions. Although the FLS contained herein are based upon what Starlight Capital and the portfolio manager believe to be reasonable assumptions, neither Starlight Capital nor the portfolio manager can assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on FLS. Unless required by applicable law, it is not undertaken, and specifically disclaimed that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events or otherwise. Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. Investment funds are not guaranteed, their values change frequently, and past performance may not be repeated.

Starlight, Starlight Investments, Starlight Capital and all other related Starlight logos are trademarks of Starlight Group Property Holdings Inc.